If you ever felt guilt about spending money (even when you have it to use) and can’t get out of a saving mindset, then this article is for you.

Do you get nervous about spending money?

I used to struggle with spending. Whether it be on a gas bill or a buying a burger.

I had a scarcity mindset. If I spent money on something I felt like it was money I could never get it back.

What If I needed that money for something else? Could I afford it? What if people judge me for what I’m buying?

Over time, I built on a few ways to improve my confidence and control with spending:

- I worked out what I loved to do

- Gave myself some guidance on how I wanted to spend money

- Challenged myself to think bigger about spending

Going through these stages, I found that I could start having fun spending money on the things I enjoy, without any guilt.

It not only shifted my mindset from scarcity to abundance but changed the way I saw money as a part of my life.

No numbers, no calculations. I want to help you feel ok to spend money.

I want to show you the path I took and explain how I went from spending money in fear to spending money and having fun.

There's something I should mention first…

Spending money can lead to more satisfaction in life

We all know money can't buy happiness, but it can buy you satisfaction.

You can be more satisfied with life more of the time by spending money on things that make you satisfied.

Could be a meal, an event, clothes, a trip. If it satisfies you then you will live a richer life.

A lot of our spending guilt builds up from not knowing if we will get value from something or that we know it won't be a good idea.

Ask yourself before you spend something. Will this satisfy me now, later or in the future?

Take action and work out how you love to spend money

If you’ve ever done a budget, you might have mapped out all your expenses and savings goals. The thing we neglect the most is our spending money, or fun money.

We sometimes consider this the leftover money. Anything that isn’t used for expenses or savings is your spending money.

This isn’t just nominating a number, but working out what exactly you want to use that money for.

So how do we do this? Here are some steps to completely owning your spending needs and habits while aligning them with your lifestyle priorities.

Let’s do a little exercise

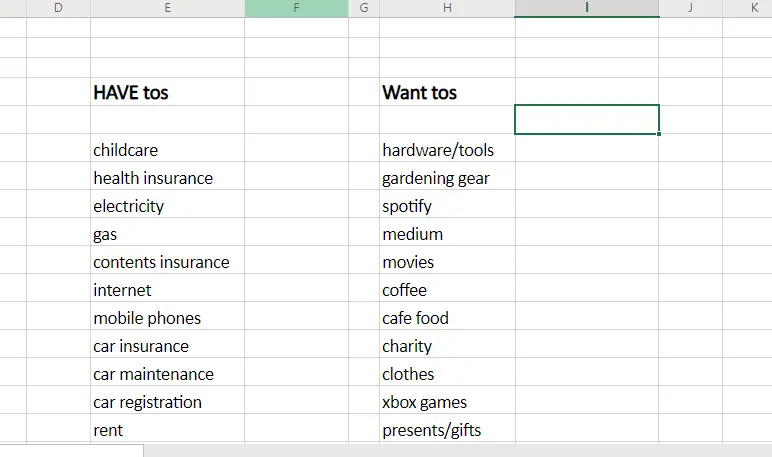

We’ll do that by listing you spending in two columns, the HAVE tos and WANT tos.

Jot down anything you’ve paid for over the last 2-3 months.

Already we now have a good understanding of what we need to spend money on and the fun stuff that chews up the rest of our spending cash.

Without thinking about how many things are, let’s keep the focus on the want to column.

Understand your money priorities

Everybody is different, and everyone has different priorities in their life.

For me, it’s family, our home, and relationships. This is the way we typically spend our money to keep these parts of our lifestyle running the way we like.

Others might spend on convenience, luxury, generosity or health instead.

We all have themes to how we spend our money, as we all have priorities of what we want in our head.

I’m calling these out because these are things we spend money on irrespective of cost. These are the things we truly enjoy spending money on.

For example:

- You like the grocery store that is more expensive as its walking distance and has better products.

- You might like to go to the more expensive gym as your workouts they put you in better health

It might not be something everyone does and is an expense we can avoid, but it is something we love doing so have little to no interest in eliminating it.

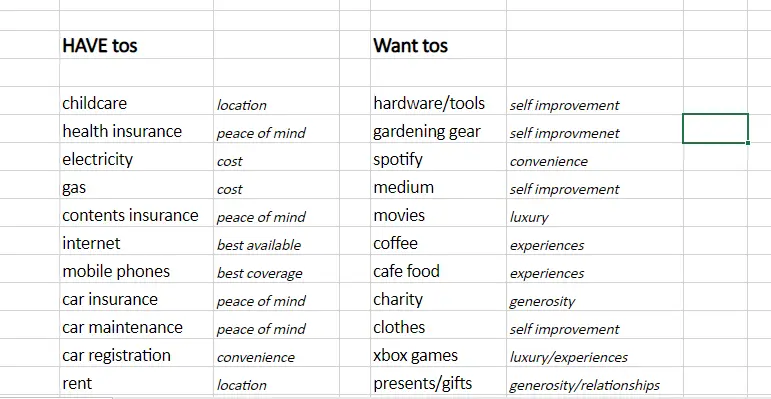

Not all your expenses need to be the cheapest. How you would categorise each of the items you’ve listed based on your reason for purchasing?

Is it by cost, convenience, luxury, health or another priority?

Here are mine in this example

Find a reason you are paying for each of your expenses to make it easier to justify the expense.

Now we have some idea of why we want to spend money on the things we buy, we can see more direction in how we do things.

Find a reason you are paying for each of your expenses to make it easier to prioritise the expense.

These steps should help you feel more comfortable with your spending habits. Everything in your spending list should have a reason it's on there.

This should align with your values and what you want to achieve. If something stands out that shouldn’t be there (you don’t want to spend money on it), then that’s what we’ll cover next

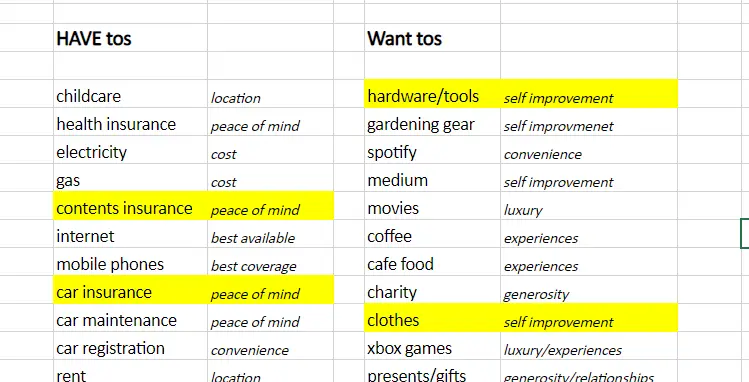

Cut mercilessly on things you don’t value

If you see anything you don’t value, then don’t be afraid to cut it out or cut back. Do this by finding alternatives to product or service.

For instance, you may spend $150 a month on lunches which might be a convenience cost, health cost or experience cost. If it’s a convenience cost (you don’t have to make it yourself) and convenience is a priority to you, then $150 is fine as you know the value in the purchase.

If you are spending the money without valuing convenience (or any other reason) then consider reducing the amount you spend and replace it with another habit or process, like making lunches a week in advance.

Highlight a few areas of spending that you do not value.

Start cutting down on the things you don’t see value in so you can align your spending with your lifestyle priorities.

Set some guiding principles to spending money

You should now have a list of what you spend your money on, how each of these costs aligns with your lifestyle and what you like to focus on and remove focus ongoing forward.

It’s not meant to be a budget as it maps out what you spend money on rather than how much. It’s meant to compliment your budget by listing out your spending habits and priorities.

For example, my family's guiding principles look like this:

- Live lean and pay for experiences over things

- Spending on health is non-negotiable

- Don’t travel often, so make sure each trip is unforgettable

- Avoid debt for as long as you can

- Don’t buy nice things while the kids are young

- Invest money every time you get paid

- I enjoy looking good and want good quality clothes

- Keep investing in yourself, through education

The list goes on but get the idea. You might also disagree with some or all of what I have. That’s ok.

Put in place some structure to how you want to spend money. It makes it easier and more transparent.

Share this with our partner or keep it printed out for reference so you don’t have a scrambling mind when you buy something.

Find new ways to think about where to spend money

Most of us got our spending habits from our parents.

Maybe they always drove brand new cars, you ate out at restaurants once a week or they never spent more than $30 on a haircut.

I’m sure you might remember a lesson or story one of parents told you about what they thought was the right way to treat money.

Those memories influence the way we think about spending money today.

I’m not here to say it was a good or bad thing, but that you have probably been heavily influenced by others in how you deal with money.

Here are four ways to think about money in the way you might not have before.

You have an optimal age to spend money

I was listening to a terrific podcast episode from Noah Kagan’s show where he was interviewing one of my favourite personal finance guru’s Ramit Sethi. Ramit glosses over a quick quote from his Uncle at around the 29:30 second mark.

He mentions a story where he was told by the Uncle

This raised my eyebrows.

I started thinking about this statement. Few people talk about spending, especially not the windows of peak spending.

For me, I thought my spending would peak when I retire. Money saved for retirement would be accessible, cost of living would be lower with (hopefully) minimal debts.

But then I thought about where I’ll be in life during my 40s. Life should be more predictable with the big phases of marriage, kids, building a career already established.

Spending on what I love in this age bracket might be more enjoyable as I have more money, better income and a clear runway of what I want to do (if things continue as they do for many).

This is in contrast to your 20s and 30s where nothing is consistent – you are going through rapid changes of work, relationships, lifestyle and circumstance.

And then the end of the window, when we get to 75. By then you’d think we’d have achieved much of what you want to do. Spending here would most likely only need to cover the lifestyle we’ve been building up. Even if we needed the cash, there should be enough in savings or assets to cover that.

Spend on yourself more

No not more clothes, food, new car, but an upgrade in what you know and can do. Your skills. Spend on education.

Upskill to become better and more able. Give yourself better luck through better education and preparation.

It’s easy to improve growing up, but not so much as an adult. We grow without trying. We are in environments where we keep moving. At the end of our formal academic education we end up as adults and from there we need to move ourselves.

This is where we neglect personal growth. It’s no longer a given we expand and learn new things, it’s easy to become stagnant.

What efforts are you making to help yourself get better this year?

I like online courses and find the paid premium ones are worth the money. Masterclass, Udemy, even online short courses from Universities.

Don’t let money be a barrier to what you want to achieve. A purchase on yourself could be the gateway to what you always wanted in career or life.

Focus on horizontal wealth

If certain things in your life already make you happy, why not spend more on them and just them?

Instead of accumulating things and counting up the stuff you have, move across and think of another way to spend money on what you already have.

This thinking can help you build horizontal wealth.

If you love driving, then spend money on improving the experience. Take a course, add some luxury, go to a related event. If one thing makes you happy already, spending more on it is ok if you continue to have fun and can afford it.

Experiment with your money

I’m a big fan of using money to find out more about yourself.

Through experiments you can test to see whether things you are dreaming about will make you happy. This can help you avoid accumulating vertical wealth by investing small, swift experiments to see if something is worth more of your money.

For example – You might have long-term goals like an extended overseas trip, early retirement, a luxury car. Something you like but have never really tried before.

For example, you might take two weeks off work if your dream is to retire early or rent a luxury car for a week if it's the one you’ve always wanted.

The idea is to give yourself a taste (and a bit of reward in the process) to work out if this is really what you want.

No point in aiming to get somewhere for a decade or more only to realise it's not even what you’d thought it’d be.

Also think of ways to use your money for experimenting with new things.

Buy that thing in the infomercial you think is useful, send someone a generous gift unsuspectingly or go for the upgrade you’ve always wondered about.

Spending money on something you might not like or enjoy isn’t necessarily a waste, it could be an experiment to see if you want to spend more on it or not.

Shift to an abundance mindset and make spending money more fun

Spending money should be something you look froward to doing. It shouldn’t bring fear or guilt. It should open up options for you to do the things you want, love, enjoy , celebrate and cheer.

It’s up to you to work what these things are and focus on them.

This article isn’t here to get you spending more often, but more on the things that mean the most to you.

To not be scared or nervous doing that .

Everyone is different, everyone has different ambitions but get clear on what your priorities are. It’s possible to train yourself to enjoy these things.

Go through and take the time to think more about how you spend:

- Work out what you love spending money on

- Consider alternative ways spending can make you better

- Improve your overall satisfaction with life

This is the process I used to flip from save, save, save to spend and enjoy.

Sometimes I just want to buy a coffee and enjoy it.